This paper will examine the impact on the apparel industry’s growth and the performance of major apparel exporting countries with special focus on Bangladesh after the phase out of the multifiber agreement (MFA) on 31 December 2004. Almost all anticipated that removal of the MFA might lead to a dramatic drop in export from Bangladesh and other Asian nations. But the facts and features are completely reverse.

Our analysis reveals that while all major apparel exporters like Italy, Turkey, France, Belgium, China, South Korea, etc lost export steam since 2008 due to the global recession especially in their export destinations despite having preferential access and geographical proximity, Bangladesh not only maintained its past gains, but also improved its performance considerably during both the post-MFA and recession periods.

This surprising growth of the Bangladesh RMG sector could be attributed to continuous support from its government, lowest wage rate, lower export price, accompanied by stable exchange rate and political stability.

Introduction

In the world, the prime concern and focus of all nations is to create power and control by enhancing economic strength. Most countries have embraced export-oriented strategies to accelerate their economic development. The best example is the Newly Industrialized Economies (NIEs) in East Asia. The high performing East Asian economies have attained high per capita growth rates, relatively low income inequality, high educational attainment, record values of domestic savings and investment, and booming exports from the 1960s to the mid-1990s (World Bank, 1993; Gereffi, 1999). Their economic achievement is largely attributed to the adoption of export oriented industrialization.

In this context, it is worth noting that textile and apparel manufacturing is the typical starter industries for countries engaged in export-oriented industrialization. These industries have been considered as important elements in economic activity and growth since the beginning of the Industrial Revolution. There are two reasons behind this concept: firstly, textiles and apparel are basic items of consumption to all; and secondly, apparel manufacture is labor-intensive, requiring relatively little fixed capital but can create substantial employment opportunities.

Thus, textiles and apparel have been major issues in trade relations among and between many countries. As a result, a large number of agreements (multilateral and bilateral), mainly between developing and developed countries, were signed over the years generally to restrict the quantities of textiles and apparel traded (Bernard A. Gelb, 2005; Joarder et al., 2010).

Bangladesh has also adopted an outward oriented trade policy, especially in the apparel manufacturing sector to accelerate economic growth. In recent years, for Bangladesh there has possibly been nothing more spectacular than the growth of its apparel export sector. The share of apparel export to total export rose from 0.5 percent in 1980-1981 to 76 percent in 2005-2006. In fiscal year 2006-2007, Bangladesh earned about $10 billion primarily from the apparel manufacturing sector (EPB, 2007). By 2013 the country’s readymade garment (RMG) sector became a $19 billion industry. Over the last decade the sector registered the significant growth of 15% while one-third of the country’s industrial labor force is employed in this sector.

The emergence and development of Bangladesh’s readymade garments industry has largely been a result of the long restricted global trade in textiles and clothing (T&C) under which the developed countries attempted to control imports through some non-transparent bilateral deals known as the Multifiber Arrangements (MFA) whereby the developed countries, i.e., the U.S., Canada, and the European Union (EU) controlled global trade in apparel. The system, on the one hand, imposed binding constrains on export potential of firms in the newly industrialized economies (NIEs) in East Asia, while, on the other hand, it provided the much needed market access facilities to the least developed countries including Bangladesh.

The policy (imposed and implemented till 31 December 2004) not only caused significant outsourcing of the labor-intensive apparel production from the relatively high-wage locations to the low-wage locations, it also unleashed a dynamic development of the global apparel value chain.

Since Bangladesh’s apparel exports grew, taking the advantage of the MFA quotas that restricted supplies from many other relatively efficient and advanced developing countries, (such as China and India) and since its supply side constraints did not show any marked improvement, there had always been a great deal of apprehension about Bangladesh’s continued success in a quota-free environment.

Prophecy Regarding the Post MFA Effect on Bangladesh

Several academic studies predicted severe consequences of the MFA phase out for Bangladesh. A study conducted by IMF economists, using a quantitative model that links different sectors and databases of cross-country trade flows, a simulation of quota-free textiles and clothing trade displayed an export loss of 25 percent for Bangladesh. Information as available towards the end of the MFA regime revealed that quota rents were much higher in other countries, and particularly in China and India, in comparison with those of Bangladesh.

Before January 2005 there had been much speculation about what would be the impact of MFA termination on the dynamic and more rapidly growing Asian apparel exporters including Bangladesh, India, Pakistan, Sri Lanka, Vietnam and China. According to Dowlah (1999), the principal external factor for the rise of the Bangladesh apparel industry was the sustained market access facility to the developed markets, under the GATT-approved Multifiber Agreement and then under the Agreement on Textiles and Clothing (ATC) as the World Trade Organization came into force in 1995.

According to Mlacila and Yang (2004), Bangladesh relies heavily on textile and clothing exports and is potentially very vulnerable to this change in competitiveness. Based on assessments of quota restrictiveness and export similarity, and an analysis of its supply constraints, the paper concluded that Bangladesh could face significant pressure on its balance of payments, output, and employment when the quotas are eliminated.

The analysis of Joarder et al. (2010) reveals that Mexico, CBA nations and CAFTA regions in the U.S. and Turkey in the EU lost their market share despite having preferential access and geographical proximity. In addition, all major apparel exporters except Bangladesh, Vietnam, and China lost their market share since 2008 due to the global recession in their export destinations. Bangladesh not only maintained its past gains but also improved its performance considerably during both the post-MFA and recession periods. This surprising and overwhelming growth of Bangladesh’s RMG sector could be attributed to the continuous support from the government, lowest wage rate, lower export price, accompanied by stable exchange rate, political stability and, above all, getting the GSP facilities for remaining in the least developed nations’ lists.

Nordas (2004) does not find an absolute decrease in total export from Bangladesh but finds a decrease in the market share of Bangladesh’s apparel in the USA (Joarder et al., 2010).

Actual Export Performance after the Phase Out

After all the negative anticipations and potential threats from home and abroad regarding the MFA phase out, Bangladesh’s staying ability and success seemed a puzzle to many analysts. In spite of some initial bumps after the MFA phase out, the apparel industry in Bangladesh managed to absorb the early shock and adjusted itself to navigate in the relatively open business environment.

According to the Export Promotion Bureau (EPB) of Bangladesh, export receipts from RMG stood at $7.6 billion in the fiscal year July 2003-June 2004. The growth rate recorded for 2005-06 was even higher at 23.5 percent with receipts from apparel exports reaching $7.9 billion. Therefore, between July 2004 and June 2006, Bangladesh’s RMG exports increased by $2.5 billion.

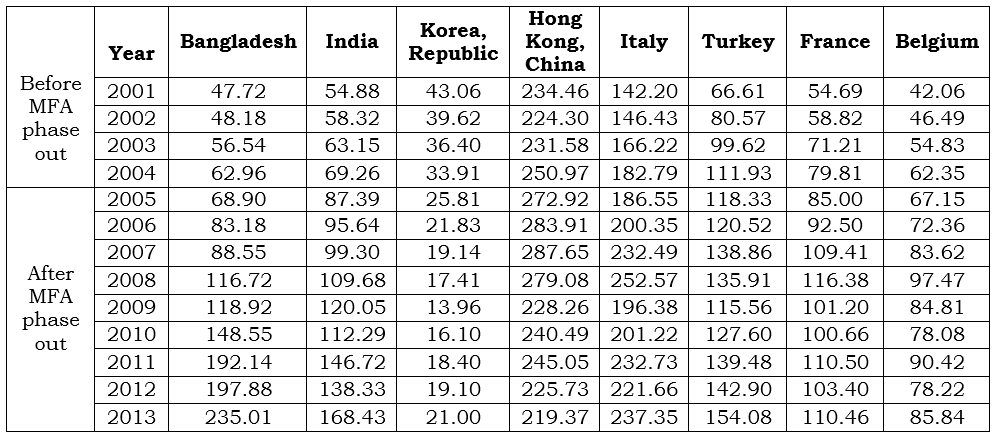

Table 1 shows data on textile export among few developed and developing countries before and after the MFA phase out. The data indicates that apart from Hong Kong – China, France and Belgium, the quantity of export to other countries has gradually increased between 2001 and 2013. Here it’s observed that an enormous shift has taken place in case of exports only in Bangladesh and India.

In Bangladesh, before the phase out export earning was not more than $6 billion while after the phase out it started to increase each year and by 2013 the amount reached almost $19 billion. This export surge shows that after the MFA phase out textile export from Bangladesh increased by more than 200 percent. On the other hand, in India and Turkey, exports after the phase out have risen approximately by 127 percent and 72 percent respectively while in Italy, France, Belgium and even in Hong Kong–China a decreasing export trend has been observed.

Source: WTO database

In 2009, after the phase out, the export volume had reduced in all countries due to common and counter effects of recession. Then again from 2010 the volume started to increase.

Table 2 shows export data in clothing before and after the phase out among the same developed and developing countries selected in Table 1. Almost all countries, except Korea and Hong Kong-China, considered here have achieved successive growth in the clothing sector after the MFA phase out. But in the case of Bangladesh exports have simply flourished. According to the data export reached $235 billion in 2013 whereas it was just around $63 billion before the phase out. Clearly, in export of clothing, Bangladesh recorded a massive 270 percent growth after the phase out.

Source: WTO database

Factors behind the Post MFA Growth in Apparel Industry

Studying the data and the circumstances it has been found that there is a strong presence of several factors due to which Bangladesh has achieved impressive success with apparel exports.

Restrictions on Export from China

After the removal of the MFA quota on January 1, 2005, the EU and the USA, the two largest export markets, imposed restrictions on certain export categories from China. These measures were imposed from July 2005 to the end of 2008. The imposition of these safeguard measures limited supplies from China and adversely affected their export volume. Statistics reveal that the exports from China to the EU in all textile and clothing categories dropped by 8% in volume during the first seven months of 2006. A similar scenario is observed in the US market. If only apparels are considered, it is found that China’s export volume to the US declined by around 7 percent during the first seven months of 2006 compared to the same period of the previous year (Cotton- Bangladesh, 2005).

This restriction on China opened a window of benefits for some other Asian countries including Bangladesh in the apparel industry. Although, during the initial period of the MFA phase out Bangladesh exports to the EU fell to 3.7 billion euro from 3.9 billion with a negative growth, it rebounded with a 38% growth during January-July of 2006 (EPB, 2007). Not only Bangladesh, but Cambodia, India, Indonesia, the Philippines, Sri Lanka, Vietnam, etc also enjoyed positive developments in their apparel sector. In point of fact, after the quota phase out Bangladesh got an opportunity to enlarge its exports of woven garments and knitwear items to the US and EU markets.

Depreciation of the Value of Bangladeshi Currency

The depreciation of the Bangladesh currency (taka) was another factor which helped the attainment of positive growth in Bangladesh’s export performance. Specifically during 2004–2007, the taka underwent a considerable depreciation against the US dollar while the Indian rupee and Chinese yuan appreciated during that time period.

So under such circumstance the depreciation of the taka along with the MFA phase out was the prime combination behind the enhanced growth of the apparel sector in Bangladesh. But continuous depreciation for enhancing exports is not a sustainable way to preserve the growth in the apparel industry. If this becomes the trend then it will definitely be a serious crisis for our competitiveness in the apparel sector in the near future.

Integration to the Global Apparel Value Chain

The Bangladesh apparel industry has maintained a relational contract with international suppliers and buyers from the very beginning, which has had a positive and lasting effect on output and labor productivity. The industry’s integration with global apparel value chain became another factor for the success of the Bangladesh apparel industry. The good quality of its products and long lasting supportive business relationship with the leading buyers in Europe and the US have helped the Bangladesh RMG industry to survive well thus far.

Indeed, even after the MFA phase out when market conditions became uncertain, Bangladeshi garment factories continued to receive orders from big buyers, due mainly to their past reliability as business partners. In some cases, buyers look at Bangladesh as an alternative source apart from the powerful suppliers. Apparently, big buyers such as Wal-Mart, H&M, Levi’s, Nike, etc. do not intend to leave the country overnight. At this stage, that helps the Bangladesh industry immensely to survive and thrive.

Offering Lowest Price of the Product

Another main reason for Bangladesh’s success in the apparel market is price competitiveness. The trend of world apparel business reveals that countries with lower wage rates always get priority to be the major apparel suppliers primarily as the industry is labor intensive. Thus in a labor intensive industry wage rate becomes the important determinant of production cost. The labor cost in Bangladesh is very low (Table 3) as it has a surplus labor force always. Hence it enjoys the ability of keeping relatively low wage rates as well as low production cost. Consequently, Bangladesh is one of the lowest price offering countries to both the USA and the EU’s 27 countries.

Source: Jasin-o’ Rourke Group, LLC; (Joarder et al., 2010)

Facilities Provided by the Government

The Bangladesh government has also initiated several support measures specifically targeting this sector. For the expansion of the RMG industry the government plays an important role by providing various policy supports at every step including bonded warehouse facilities, duty drawback incentive, cash compensation scheme, stable exchange rate, lower export price and the facility of procuring raw materials.

Future of Apparel Industry in Bangladesh

The apparel industry in Bangladesh now has become the most successful sector as it holds the major share of the total export volume of Bangladesh. Unfortunately such an important sector for Bangladesh’s continued success has been suffering from some problems.

Labor Issue

The main issue for our apparel industry is the violent labor unrest and the subsequent upward adjustment of wages proposed. There is no denying that the RMG industry has long been characterized by a wide variety of deprivations of its workers, which include, inter alia, lack of proper infrastructure facilities and safety at workplace, non-compliance with minimum wages, and lack of provision of essential service benefits to the workers. Violent protests by the workers have been an outburst of their long denied basic demands.

Political Turmoil

Apart from labor issues, political disturbance within the country is another prime headache functioning against growth in the apparel sector as well as in the entire economy. Political mayhem is often manifested in countrywide strikes and blockades. During such situations production, distribution, etc all are disrupted. Moreover world geopolitics is also a matter of concern as it is sometimes suspected that labor violence is instigated by more developed and rival countries in order to hamper the consistent trend in apparel export.

Inadequate Infrastructure

It’s a matter of huge embarrassment that Bangladesh has failed to construct a proper infrastructure for its industrial development. Frequent power outages, inefficient ports and inland transportation, delayed shipment, lengthy and cumbersome procedures in the customs related activities, damage of goods while loading and unloading and high costs of doing business, etc are the obstacles that can hinder continuous export success. All the factors mentioned above should be solved to maintain the growth of the apparel industry that Bangladesh has been enjoying, otherwise this development might turn into a short happy episode only.

Policies to Be Executed For the Well Being of the Apparel Industry

There have been significant changes in the post-MFA phase in the RMG sector in terms of technology absorption and innovation, sourcing of inputs, marketing structure and strategy, wage pattern and labor adjustment, rate of return, and state of compliance (CPD, 2007). Moreover the sector is facing new challenges as it is struggling with some undesirable problems. For strengthening the competitiveness of the RMG sector, Bangladesh needs to walk a long distance. Some policies should be developed and applied for preserving a better infrastructure and environment for this vital industry.

Enhancement of Labor Productivity

Labor productivity in Bangladesh is very low ($1563) compared to other competing countries such as China, Cambodia, India, Indonesia and Sri Lanka. Labor productivity is highly correlated to wages; one unit rise in wage is expected to increase labor productivity by 1.3 units. This implies the significance of the implementation of the new wage structure (CPD, 2007). A few elements are necessary to develop productivity, such as

- Appropriate training

- Improvement of compliance situation

- Entertainment facility

- Performance incentives, and

- Good behavior towards workers.

Ensure the Implementation of the New Wage Structure

It is now essential to implement the proposed wage structure to reduce frequent labor violence which is the biggest threat to the apparel sector. As per the recommended wage structures, the minimum wages in the industry would increase by about 80 percent. According to the labor law and act of government, the RMG work is categorized into seven grades and the minimum wage for the seventh grade worker is BDT 5,300 while for the first grade worker it is BDT 13,000 (ministry of labor and employment, 2013).

The implementation of a new wage structure would increase the total production cost. The CPD (2007) anticipated an additional annual expense of about $14,000. Hence the profit margin would also be a bit lower in the short term. But higher wages are also positively related to better working environment, better compliance and improved living standard. So in the near future it would start to generate positive returns in the economy. The government should provide necessary welfare facilities and social security to the RMG workers for the betterment of their livelihood.

Improvement of Existing Laws and Regulations

Bangladesh requires more flexible working hours with provisions for work during the night shift, recruitment of young workers as apprentices, etc. The government should be stricter on laws for improvement of worker’s health and safety standards in the workplace; regulations to change the building codes for improving working conditions, and for ensuring compliance with factory laws, etc. Various acts related to labor law, such as working hours, punishment for failing to provide maternity leave, retirement benefit of workers, timely payment of fired workers, etc. need to be reviewed (CPD, 2007).

Acquisition of New Technology

The use of various types of advanced knitting machines against the flat knitting machine should be increased and similarly in sewing operations the share of automatic sewing machines against non-automatic sewing machines should also be raised. The government should facilitate import of modern knitting and sewing machinery for the RMG sector in Bangladesh. Also the tax and VAT on importing such machinery should be lowered and made flexible to promote modern technology usage in this sector for massive development.

Promoting Labor Absorption through Technology Upgradation

Though new machines require more skilled labor for their operation, technological advancement creates new job in areas like merchandising, marketing, commercial and engineering. So it’s necessary to provide both higher and technical education in the country focusing on both new entrants and professionals in the sector to promote skilled workers.

Ensuring Uninterrupted Electricity Supply for RMG Units

Electricity problem should be attended and improved immediately. The government has taken some measures to address the power supply problem which include economizing its use, fixing sequential holidays for factories in different industrial/commercial zones, setting up small scale power generation plants, etc. The government should also source solar energy usage or the latest technological alternatives for electricity production. Eco-system operations and promotion of green production can play an effective role. Creating power from wastes of the factories can be an environmental friendly approach for assisting uninterrupted power supply to the industry.

Development of Backward Linkage Textile Sector

The government has also taken various fiscal measures to increase investment in the backward linkage textile sector. In the national budget for 2008, about Tk 8.48 crore has been allocated for three different projects for the development of the textile industry, with a view to promoting integration with the RMG sector (CPD, 2007). However, proper policies should be adapted and implemented to ensure the appropriate utilization of this fund. The sector is still dependent on import of knit, woven and dying materials which needs further improvement so that maximum sources of these items can be made or sourced from our own country.

Overhaul Port Management

For the improvement of the efficiency of Chittagong port, the Caretaker Government had taken several initiatives which included three-shift workday for dockworkers for ensuring round the clock operation at the port; reduction of container handling charges from BDT 4000-5000 to BDT 1200; handing over cargo handling activities of the different jetties in general yards to private companies; shifting handling activities of nine bulk items outside of the port area; allowing delivery of Full Container Load (FCL); reducing the size of the labor groups; setting up sector-wise off-dock inland container depot (ICD); cancellation of unreasonable fees and charges by shipping agents and reducing the number of signatures required from customs and port authorities for clearing papers; prescheduled berthing system with effect from August, 2007, etc. To speed up handling activities, the government could allow loading of containers at factory premises instead of loading goods at the port (CPD, 2007).

Concluding Remarks

Removal of quotas in 2005 has brought economic gain for some developing countries and loss for some. Among the South Asian countries, the post-MFA performance of India and Pakistan has been reasonably good. Bangladesh has achieved impressive growth, particularly in low-cost labor-intensive categories of the RMG sector. A combination of global opportunities, managed trade under the MFA and GSP facilities, low labor cost, and government support had combined to stimulate the emergence and success of the export-oriented apparel sector in Bangladesh (Joarder et al., 2010).

The post-MFA outcome that the RMG industry in Bangladesh attained in terms of export growth reflected the conjecture of the present study that the industry anticipated changes in the global market environment. In other words, the apparel firms did not merely operate in a protected environment rather made dynamic progress across products, customers, and regional markets in order to deepen their market position and sustain their profitability. If the government becomes successful in reducing the obstacles still faced by the RMG industry by implementing necessary policies and measures, only then can we ensure a sustainable growth in the apparel industry and as well as the total economy.

Very informative article….beautifully written